What owner financing actually means

Owner financing — sometimes called seller financing — is a way to buy land in which the seller carries the note instead of a bank or mortgage company. You sign a promissory note and a deed of trust directly with the seller, agree on the terms, and make your payments to the seller rather than to a lender. There is no third-party mortgage to apply for and no bank underwriting standing between you and the land.

It's a long-established way to buy rural property in Texas, and it's especially common with ranch and recreational tracts that many traditional lenders are reluctant to finance. Because the seller is the one extending credit, the seller sets the structure of the deal directly with the buyer at the contract stage.

Why buyers choose it

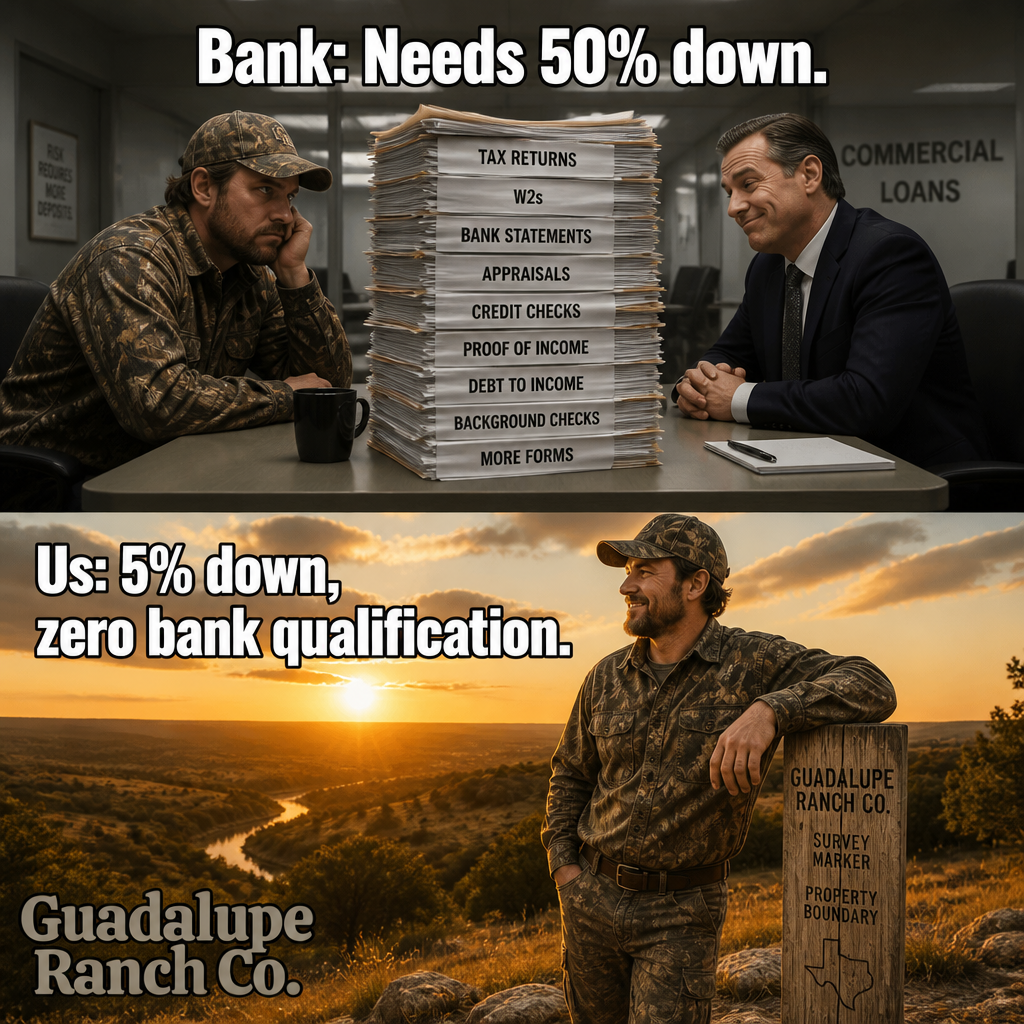

The biggest draw is that there's no bank qualification process. Many banks shy away from raw, unimproved, or recreational land because there's no house to appraise and no rental income to underwrite. Owner financing sidesteps that entirely, which opens the door for self-employed buyers, buyers who'd rather not pull their credit through a full mortgage application, and anyone who simply wants a more direct path to owning land.

It also tends to close faster. Without a bank appraisal, formal loan underwriting, and a lender's closing timeline, the deal moves at the pace the buyer and seller set. For buyers who've found the tract they want, that speed and simplicity is often the deciding factor.

The pieces of the deal: down payment, rate, and term

An owner-financed purchase generally comes together around three pieces: a down payment, an interest rate, and a term (the length of the loan). These are agreed to up front and written into the contract, and they vary from one tract to another. We don't quote fixed numbers here because the right structure depends on the specific tract and the deal — so the honest answer is that the down payment, rate, and term are set at contract, and you should ask us for current details on the tract you're interested in.

What matters to understand going in is that these terms are negotiated and documented before you close, not left vague. Once you and the seller agree, the numbers are fixed in the note so you know exactly what your payment is and how long you'll be making it.

What to expect at closing

Every tract we sell is surveyed, so you'll have a defined boundary and acreage before closing rather than a vague description. At closing you'll typically see the survey, the deed that conveys the property to you, and the promissory note and deed of trust that spell out your financing terms. Closings are commonly handled through a title company, which records the documents and keeps the paperwork clean.

Because the land comes with deeded access on graded ranch roads and carries only light restrictions, you'll know how you reach the tract and what you can do with it before you sign. If anything about the documents or the process is unclear, ask — a good closing is one where the buyer understands every page.

We're the seller and the lender

At Guadalupe Ranch Co. we service our owner financing in-house through Ranch Enterprises Loan Servicing. That means we're both the seller and the lender on the same deal. There's no broker handing you off to an outside finance company, and your payments and account are handled by the same family of companies that sold you the land.

At Guadalupe Ranch Co. we service our owner financing in-house through Ranch Enterprises Loan Servicing. That means we're both the seller and the lender on the same deal. There's no broker handing you off to an outside finance company, and your payments and account are handled by the same family of companies that sold you the land.

Keeping financing in-house keeps the relationship simple and the line of communication short: one team that knows the tract, the note, and your account. If you're weighing an owner-financed purchase, reach out and we'll walk you through the terms available on the tract you have your eye on.